Article from

What Does an Employee Cost Me? Calculating the Internal Hourly Rate.

How profitable are my projects? What do I really get out of the offered hourly rate?

Having a rough idea of these figures is important to avoid 'shooting in the dark' in business. In this case, it's about how much an employee costs per hour. Sure, one could create tables and calculate everything meticulously. But who's really into that – and is it even worth the effort? We say 'No' and would like to show how to pragmatically and tangibly achieve the goal.

English image not yet available...

English image not yet available...The Benefit of the Internal Hourly Rate

The internal hourly rate allows for solid statements to be made in everyday work – especially regarding the profitability of a project. Because the costs that a project incurs are not only made up of expenses for external services or incidental costs – there are also costs for the employee while they are working on the project.

For this reason, one should not forget to compare the overall costs with the revenues.

Calculating What an Employee Costs Per Hour

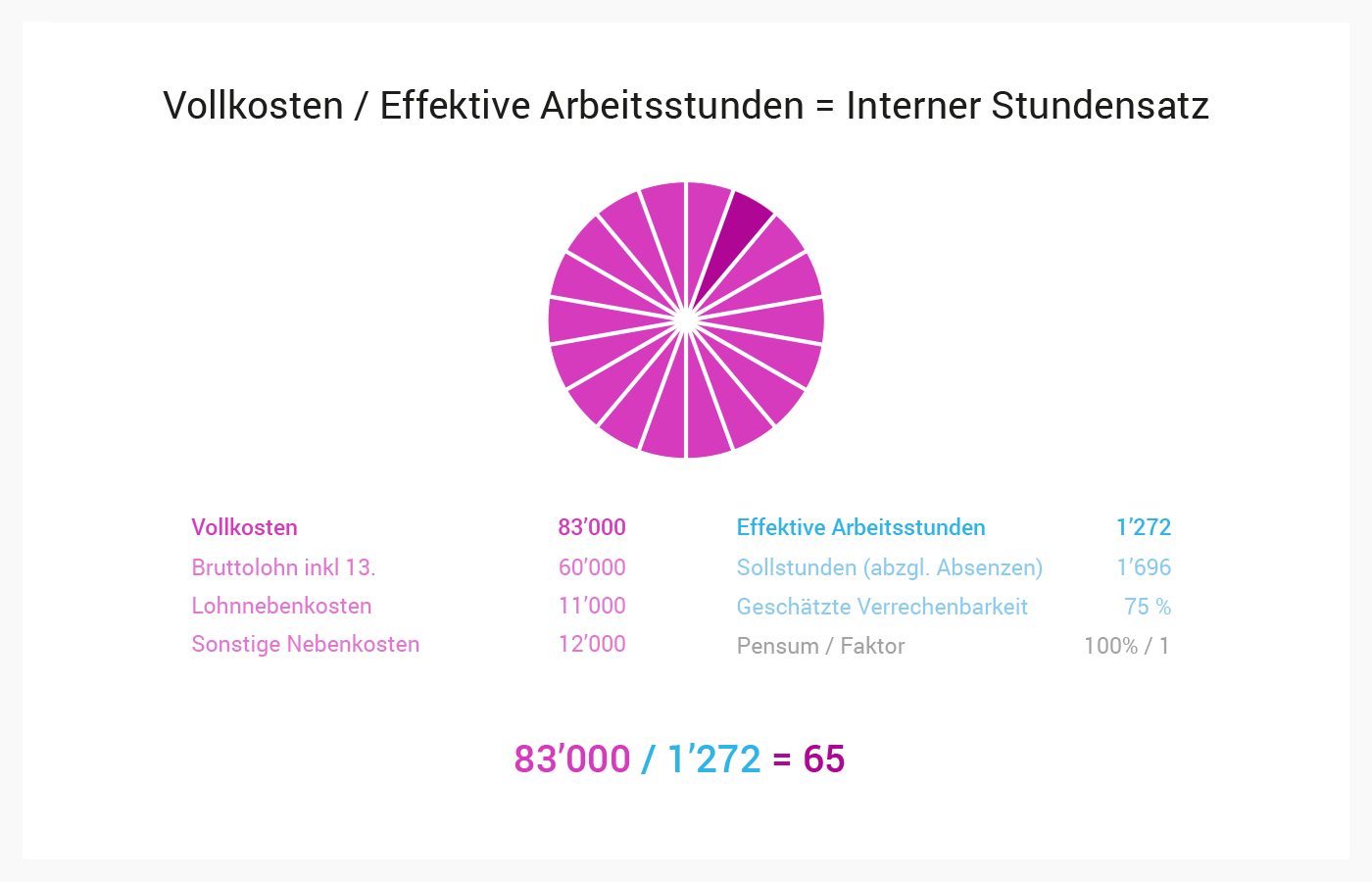

Firstly: The internal hourly rate will never be an exact number. We are looking for a number that doesn't need to be constantly adjusted, that is easily graspable and can withstand slight fluctuations. The simplest formula is:

Full Costs

Include all wage costs and other incidental costs that increase per employee. In principle, one could also allocate office rent, but that is usually a recurring amount that unnecessarily complicates the calculation. The full cost calculation consists of:

→ Annual salary (incl. 13th month, assumed bonus, etc.)

→ Payroll taxes

→ Other incidental costs that increase per employee (administration, workplace costs, management costs, office supplies, coffee & beverages)

Actual Working Hours

When it comes to the actual hourly rate, the question is how many billable hours the employee actually works.

It makes sense to rely on a general average value for the calculation. Because not every year has the same number of public holidays. Other criteria also contribute to a varying number of working days per year. In general, one can rely on the following benchmarks:

Full Costs

Include all wage costs and other incidental costs that increase per employee. In principle, one could also allocate office rent, but that is usually a recurring amount that unnecessarily complicates the calculation. The full cost calculation consists of:

→ Annual salary (incl. 13th month, assumed bonus, etc.)

→ Payroll taxes

→ Other incidental costs that increase per employee (administration, workplace costs, management costs, office supplies, coffee & beverages)

Actual Working Hours

When it comes to the actual hourly rate, the question is how many billable hours the employee actually works.

It makes sense to rely on a general average value for the calculation. Because not every year has the same number of public holidays. Other criteria also contribute to a varying number of working days per year. In general, one can rely on the following benchmarks:

Working days per week | 5

Working weeks per year | 52

Working days per year | 260

Public holidays on weekdays | 10

Vacation days | 30

Sick days | 5

Other absences | 3

Total working days | 212

Working hours daily | 8

Total working hours | 1’696

→ Target hours after deducting absences: 1’696

In MOCO: Set up a weekly model, enter public holidays and deduct the vacation entitlement and assumed sick days from the sum of target hours specified in "Target-Actual". If you have been with the company for a full calendar year, you already have this number calculated.

Working weeks per year | 52

Working days per year | 260

Public holidays on weekdays | 10

Vacation days | 30

Sick days | 5

Other absences | 3

Total working days | 212

Working hours daily | 8

Total working hours | 1’696

→ Target hours after deducting absences: 1’696

In MOCO: Set up a weekly model, enter public holidays and deduct the vacation entitlement and assumed sick days from the sum of target hours specified in "Target-Actual". If you have been with the company for a full calendar year, you already have this number calculated.

To account for unproductive times, finally deduct e.g. 25% from the calculated working time. Unproductive times include, for example, meetings, one-on-one conversations, internal training, or for managers, time spent on management tasks. The result for a full-time employee:

→ Actual working hours per year: 1’272

Tips

Tend to calculate conservatively

For incidental costs and utilization, it is better to calculate a bit more conservatively and thus be on the "safe side" rather than having the numbers look too good.

Change with higher salary

Practical are rough figures. Contrary to some assumptions, the internal hourly rate often changes only insignificantly with an increased salary. There are some fluctuations that can never be taken into account exactly. Sometimes, for example, the utilization is better or worse.

Average value at level or team level

Ideally, one should store an average internal rate for all employees at the same level even if the salaries differ slightly. This way, one does not have to worry that individuals will try to deduce salaries from internal hourly rates.

You can record the internal hourly rates in MOCO in the settings under "Services" > "Internal Hourly Rates"

For incidental costs and utilization, it is better to calculate a bit more conservatively and thus be on the "safe side" rather than having the numbers look too good.

Change with higher salary

Practical are rough figures. Contrary to some assumptions, the internal hourly rate often changes only insignificantly with an increased salary. There are some fluctuations that can never be taken into account exactly. Sometimes, for example, the utilization is better or worse.

Average value at level or team level

Ideally, one should store an average internal rate for all employees at the same level even if the salaries differ slightly. This way, one does not have to worry that individuals will try to deduce salaries from internal hourly rates.

You can record the internal hourly rates in MOCO in the settings under "Services" > "Internal Hourly Rates"

Conclusion

The internal hourly rate as a pragmatic benchmark allows for solid statements to be made in everyday work. Revenues minus variable costs are also referred to as "Contribution Margin 1". The question 'How much does this project bring us' is to be answered with this. From this amount, the company's fixed costs must then be paid. The number does not differ as much as is often assumed with different salaries, as there are fluctuations besides the calculable factors.